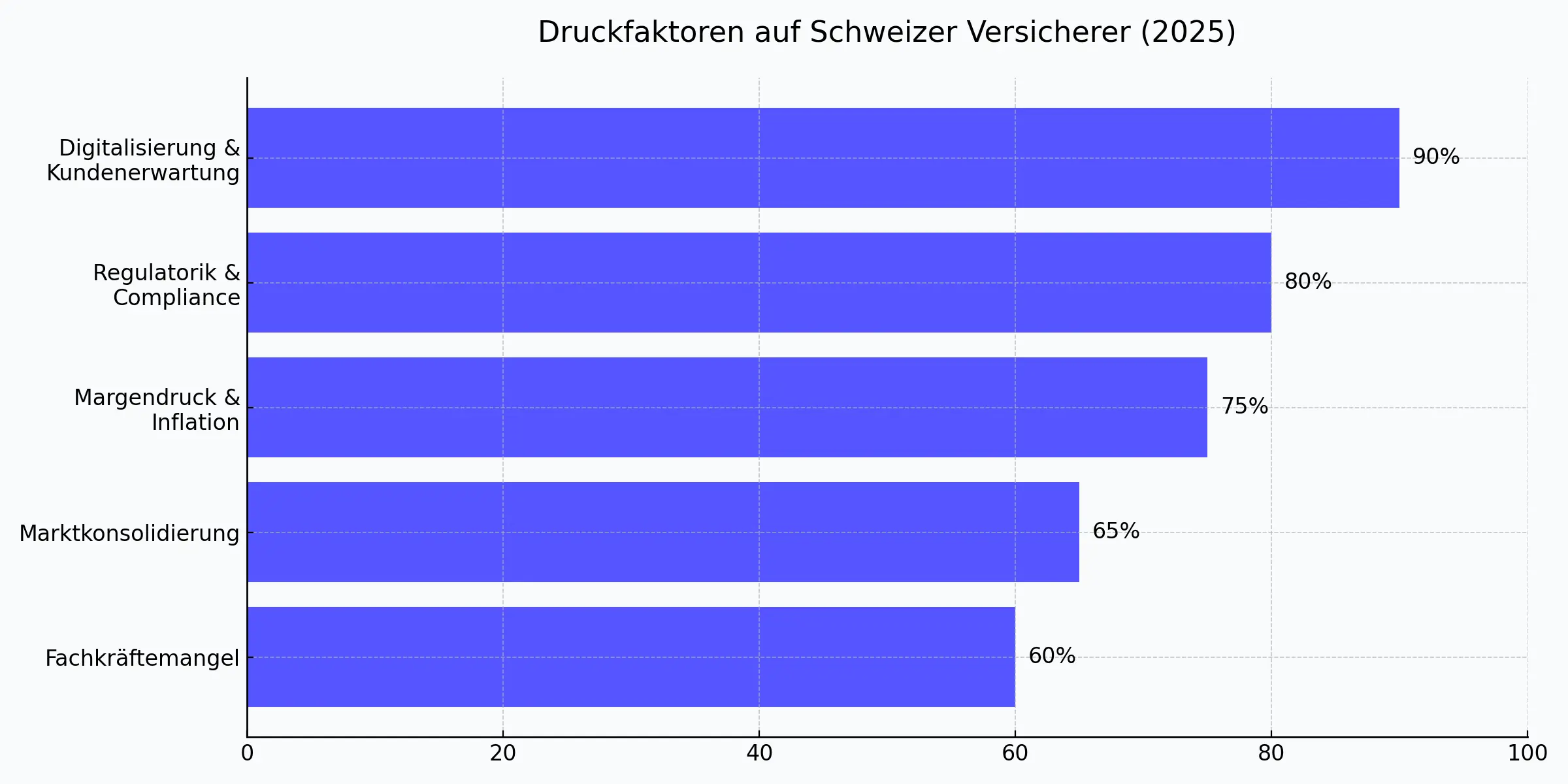

The Swiss insurance industry is under massive pressure to change. While customer expectations are rising, technological innovations are setting new standards and regulatory requirements are becoming more complex, one central challenge remains: How can processes in the insurance industry be made more efficient without sacrificing quality or customer proximity?

In an interview with HZ Insurance Marcel Thom from Deloitte sums up the situation: "The pressure for greater size and efficiency is increasing significantly." The planned merger of Helvetia and Baloise is only the most visible signal of a far-reaching structural change. One that has long since also reached medium-sized and smaller market players.

It is no longer just about reducing costs. Today, efficiency is a strategic competitive factor. It determines whether insurers can react quickly to market changes, whether customers are satisfied across all channels and whether internal resources are deployed in a targeted manner.

This article sheds light on the causes of efficiency pressure, analyzes the biggest weaknesses in the current operating model of many insurers and shows practical ways in which organizations can now take countermeasures - technologically, procedurally and culturally.

1. why the topic of efficiency belongs on the agenda now

The Swiss insurance landscape is traditionally characterized by stability, long-term customer loyalty and proven business models. However, this starting position is increasingly being shaken - not only by technological developments, but also by convergent pressures:

1.1 Consolidation as a wake-up call

The announced merger of Helvetia and Baloise is more than just a market novelty - it is a symbol of a new reality. Economies of scale, synergies and greater scope for investment make it clear that those who do not follow suit will struggle to remain competitive in the medium term. Small and medium-sized insurers in particular are faced with the question of whether they have their processes under control - or whether structural inefficiencies will choke them off in the long term.

1.2 Digitization: from option to necessity

Many companies have launched digitization projects, but these often remain pilot projects or isolated solutions. However, customers have long expected more: fast processing, digital services and constant availability. The pandemic has also shown how dependent many insurers still are on manual procedures and paper-based processes. Those who do not catch up here will lose not only efficiency, but also relevance.

1.3 Margin pressure and claims inflation

Added to this are economic factors: increased repair costs, more expensive medical services, more frequent severe weather events. Claims inflation is forcing insurers to keep their costs under control without driving the premium burden to infinity. Efficiency is therefore becoming the key factor for economic stability.

1.4 Regulatory requirements

At the same time, the requirements for reporting, compliance and data protection are increasing. These tasks are non-negotiable, but they tie up resources. Automating and data-driven processes frees up time for more strategic tasks.

2. where the inefficiencies really lie today

Most insurers would not describe themselves as inefficient, and this is true at first glance. Processes run, policies are managed, claims are processed. But a closer look shows: In many companies, there is still a strong operational dependency on manual activities, isolated systems and personal knowledge. This is precisely where the problem lies.

2.1 IT legacy: complex, expensive, cumbersome

Many insurers operate with historically grown IT landscapes. Systems that are not integrated, processes that run twice, interfaces that are prone to errors. This not only makes innovation more difficult, it also costs time and money on a daily basis. A simple example: claims are reported digitally, but internal approval is still done by email and PDF.

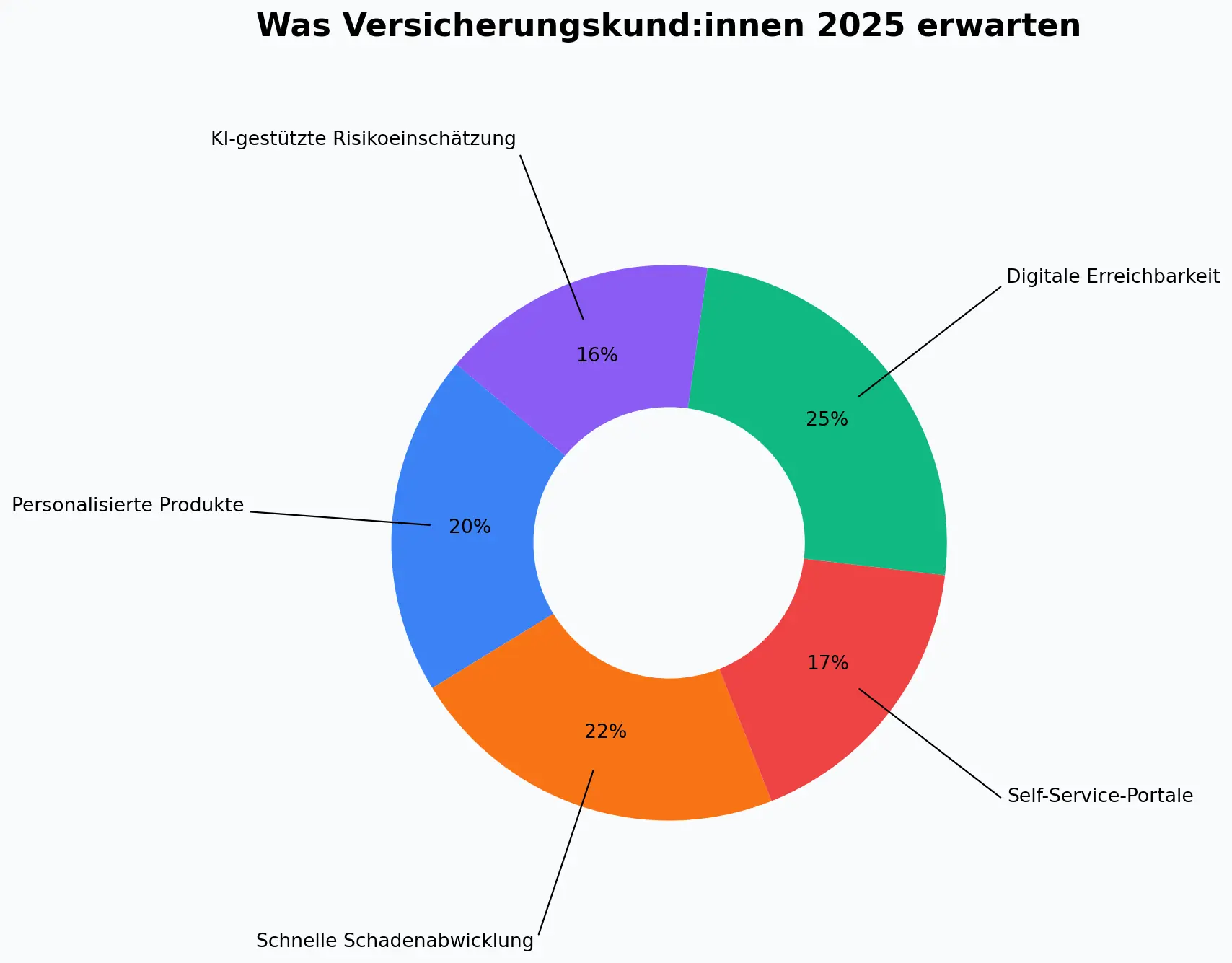

2.2 Media disruptions in the customer process

A customer starts their journey on the website, wants to make an appointment or adjust a policy, and is then called back by phone or asked to fill out a PDF. Such media disruptions lead to frustration, unnecessary effort and bounces. At the same time, they massively increase the internal workload because information has to be updated manually.

2.3 Inefficient internal cooperation

Coordination between sales, underwriting and the claims department is often informal: by email, telephone or in endless meetings. Roles are not clearly defined, responsibilities are blurred and processes are dependent on individual people. This paralyzes speed and scales poorly.

2.4 Underestimated wealth of data

Insurers are sitting on a treasure trove of data - but many hardly use it. Reports are created retrospectively, decisions are based on experience instead of real-time data. AI and analytics could help to assess risks more precisely, optimize processes and enable real personalization.

2.5 Deceptive customer satisfaction

According to Deloitte, over 80% of Swiss customers are satisfied with their insurer - but more than 75% never review their policies. Satisfaction does not equal loyalty, but is often an expression of a lack of alternatives. This leads to a deceptive sense of calm that masks the pressure to change.

3. strategies to increase efficiency - with practical relevance

Efficiency is not a project that can be ticked off with a new tool or a process definition. Rather, it is about a fundamental change in the way insurers structure their internal processes, use technology and design customer experiences. If you want to survive in today's market reality, you have to ask yourself honestly:

Which processes create value, and which are pure friction?

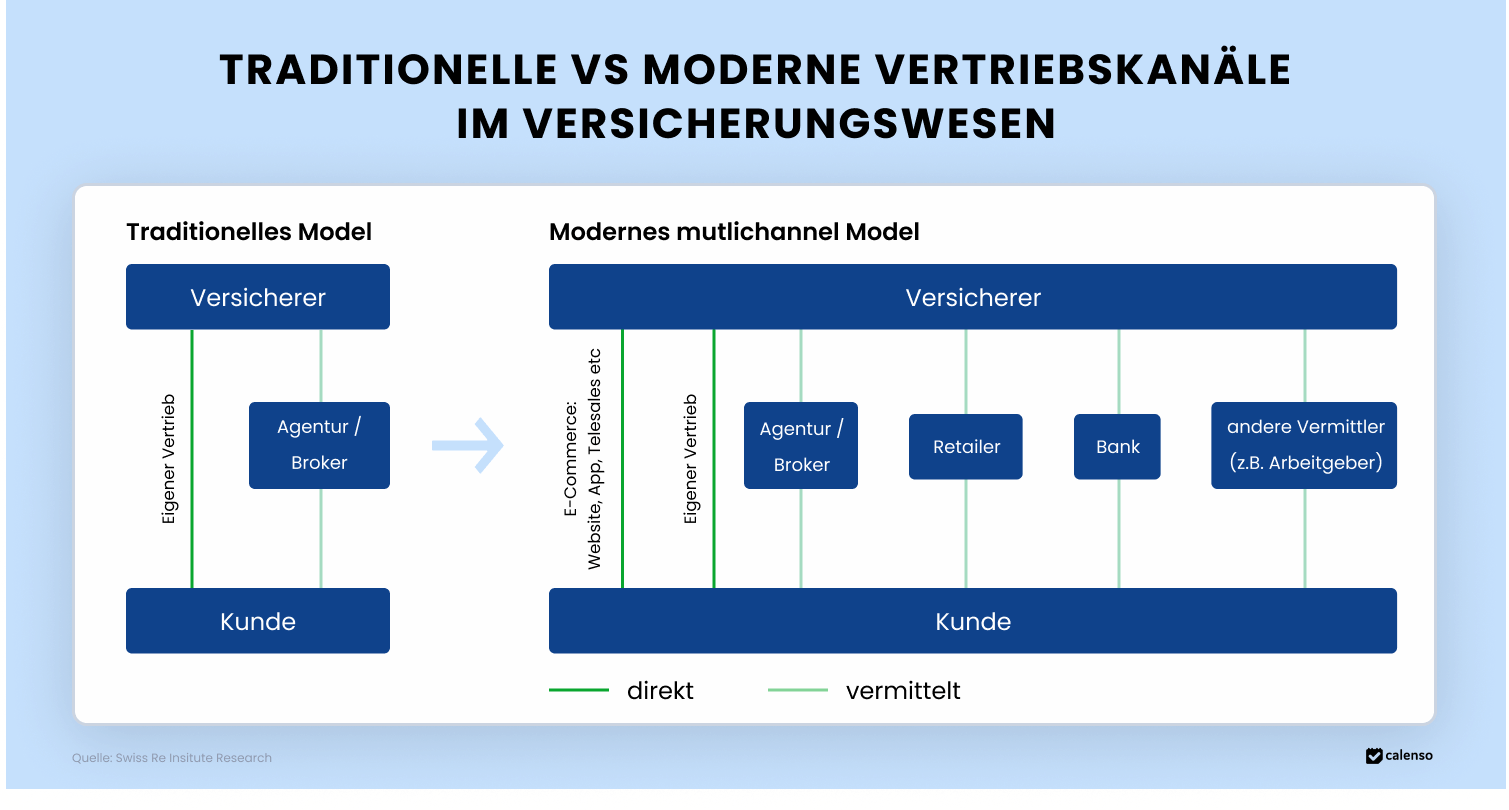

3.1 Cloud & API-First: Foundation for speed and scalability

The cloud is much more than just an infrastructure issue. It forms the basis for a modular, future-proof IT architecture that can grow with the requirements of the market. While monolithic systems used to turn every change into a lengthy IT project, modern, API-based platforms now enable third-party applications to be connected quickly, from AI modules to self-service portals.

But the efficiency gains go deeper: cloud solutions reduce maintenance costs, simplify updates and improve reliability. At the same time, they enable specialist departments to react more quickly to new requirements without having to wait months for IT resources. Those who think cloud-first also think in terms of processes, not just systems.

3.2 Automation and AI: from pilot to productive solution

Numerous insurers are experimenting with AI, for example in the analysis of claims patterns or risk assessment. However, only a few have made the step to real operationalization. Yet this is precisely where a decisive lever for increasing efficiency in the insurance industry lies: automated processes reduce throughput times, minimize sources of error and relieve employees of repetitive tasks.

A practical example: If a claim is automatically categorized, compared with historical data and, in the case of low complexity, approved directly, manual intermediate steps are no longer necessary. The result: faster processing, fewer queries, higher customer satisfaction. In this context, efficiency does not mean sacrificing human expertise, but rather a targeted reduction in the workload of the most valuable resource: employees.

3.3 Omnichannel communication: efficiency starts with the customer experience

In an ideal world, every employee knows what the customer last discussed, whether by email, phone or chat. In reality, however, many customer interactions end up in a "channel silo". What was started in the chat has to be explained again on the phone. The insurance seems fragmented, the customer repeats himself, the internal effort increases.

Well-orchestrated omnichannel communication solves this problem not just on the surface, but structurally. When systems and teams work together seamlessly, end-to-end processes are created with fewer media disruptions. Customers receive answers where they expect them and employees work with full context. The efficiency gains are doubly noticeable: less internal coordination, more customer satisfaction.

3.4 Self-service and digital autonomy: relieving the burden of responsibility

Many insurers underestimate how willing their customers are to do things themselves, as long as they are simple, easy to understand and can be done at any time. Anyone who wants to report a claim, book an appointment or change an address doesn't want to do this using a form or hotline, but intuitively and in seconds.

Digital self-service platforms enable precisely this, while also reducing the administrative workload on the company side. Where customers can resolve their concerns independently, the number of manual inquiries is reduced. The resources freed up can be used more specifically for complex consultations, claims settlements or product development.

4. human success factor, process efficiency requires cultural change

Technology alone does not make an efficient company. Many insurers invest in systems, tools and platforms, but if the internal attitude remains the same, the effect fizzles out. Real efficiency can only be achieved when processes, technology and people work together.

A central problem: processes have often grown historically, not in the interests of the customer, but in the interests of the organization. Employees learn to live with complexity, develop workarounds and thus unintentionally contribute to maintaining inefficient processes. If you really want to become more efficient, you need to have the courage to fundamentally question things and actively involve employees in this change.

This is because change generates resistance, especially when it comes across as a technocratic top-down project. Successful insurers manage to involve their teams at an early stage, use training as a strategic lever and not only introduce new tools, but also make them usable. The point is not to impose technology, but to make its benefits tangible in everyday life.

At the same time, new forms of collaboration are needed: silos between specialist departments and IT must be broken down, responsibilities clearly defined and responsibilities distributed. Business and technology must not be seen as opposites, but as a shared sphere of activity. This is the only way to create solutions that are not only technically sound, but also operationally relevant.

And last but not least, the shortage of skilled workers plays a role. Efficient digital working requires not only new systems, but also new roles and skills. Insurers that offer modern working models and clear career paths not only gain efficiency, but also an advantage in the battle for talent.

5. how modern tools help with implementation (very practical)

The challenge with any efficiency initiative is not the "what", but the "how". The goals are usually clear: simplify processes, reduce costs, serve customers better. But in practice, progress often fails due to an invisible opponent: complexity. Too many systems, too many dependencies, too many manual interventions.

This is where modern SaaS solutions come in. Not as a panacea, but as targeted tools to relieve existing structures. They help to digitize processes where it is most beneficial: in interaction with customers, in coordination between departments, in the automation of repetitive tasks.

One example: digital appointment scheduling in sales or in the event of a claim. What used to be a chain of answering machine, callback, email coordination and internal calendar approval can now be organized with just a few clicks, synchronized with CRM, available via all channels, automated with reminders.

Or the case of customer-initiated self-service: instead of sending a form every time there is a change of address, the customer can update their data independently and correctly. No queries, no returns, no internal tickets.

Such solutions are no utopia, but have long been a reality if they can be seamlessly integrated into the existing IT landscape and do not run as parallel shadow processes. It is not just the technology that is important here, but also the approach: modular, API-based, user-centered.

Tools such as Calenso are used in this context, not as a dominant system, but as a flexible component in the overall picture. Insurers use such solutions to achieve selective efficiency without replacing existing core systems. The idea: start small, work quickly, scale sensibly.

6. efficiency as a strategic advantage, not as a savings program

Increasing efficiency in the insurance industry has long since ceased to be a question of cost discipline or process optimization in the traditional sense. It is about much more: future viability, speed and responsiveness in a market that is undergoing structural change.

The consolidation of large providers such as Helvetia and Baloise shows where the journey is heading: economies of scale, investment capacity and digital expertise determine who can and who cannot compete. But even without mergers worth billions, insurers can make tangible progress today if they have the courage to question the old and consistently implement modern, integrable solutions.

Efficiency does not necessarily mean that fewer people work more. On the contrary: well-used technology relieves employees, reduces operational friction and creates space for what insurance is all about: trust, proximity and relevance.

Insurers that invest in process clarity, digital interfaces and an open corporate culture today will not only become more efficient. They are becoming more resilient, more attractive for talent and more relevant for their customers.

Or as Marcel Thom aptly put it in an interview:

"Especially in a saturated industry, you have to reinvent yourself before others do."